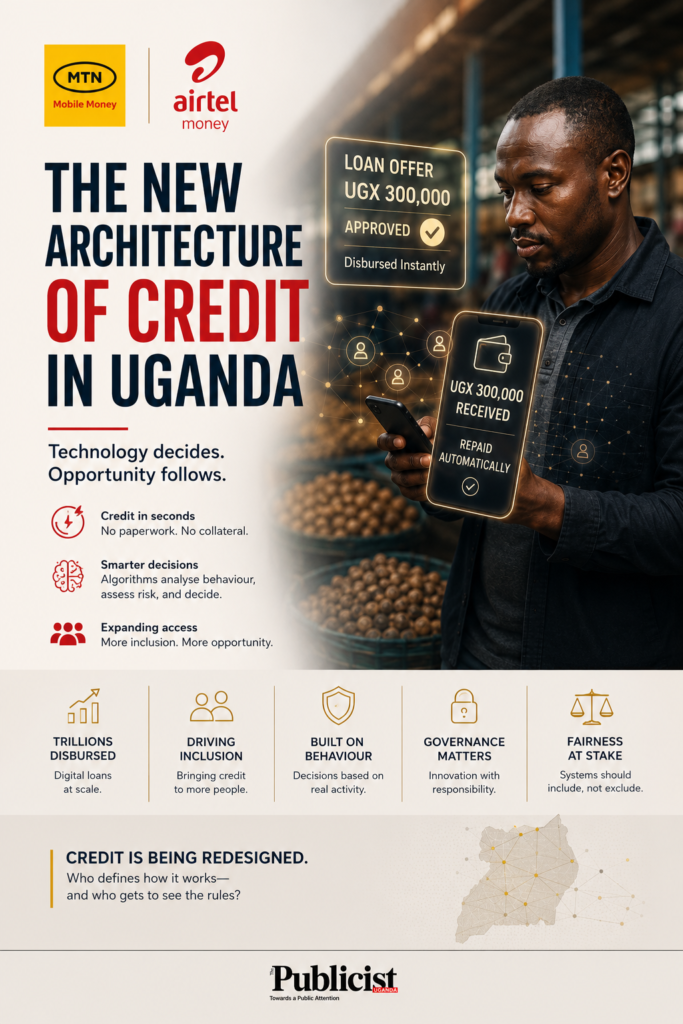

In Owino Market in Kampala, a trader named Tendo does not visit a bank. He has never filled in a loan application form. He does not own land to offer as collateral. But last Tuesday, his phone buzzed with an offer of UGX 300,000 in working capital. He accepted in two taps. The money arrived in seconds, and by Friday it had been repaid automatically.

What Tendo does not know is what decided he was creditworthy. An automated credit scoring system, running behind mobile money infrastructure, had been observing his transaction behaviour over time. It tracked spending patterns, airtime purchases, repayment history, and cash flow rhythms. It built a profile, calculated risk, and triggered an offer. No loan officer intervened at the point of disbursement.

This is the new architecture of credit in Uganda, where lending decisions are increasingly made through automated systems embedded in mobile money platforms.

The scale of this shift is significant. Mobile money platforms now disburse trillions of shillings in digital loans, with telecom operators dominating the segment. MTN Mobile Money is the largest player, while Airtel Money continues to expand its credit offerings at a smaller scale.

Across the sector, digital lending has expanded alongside mobile money adoption. MTN’s fintech business has become a core pillar of its financial services strategy across Africa, with large volumes of lending processed through its BankTech infrastructure.

This growth is happening in a context where Africa faces a large credit gap estimated in the hundreds of billions of dollars by development finance institutions. Digital lenders are increasingly using mobile transaction data to close that gap.

At the same time, Uganda’s regulated banking sector has grown more slowly, with single-digit credit growth in recent reporting periods according to Bank of Uganda data. The result is a widening divide between traditional banking and digital credit systems.

The term “AI credit scoring” is often used to describe these systems, but it does not fully capture their structure. Traditional credit scoring produces a recommendation that is reviewed by a human. In Uganda’s mobile lending ecosystem, credit decisions are increasingly automated using machine learning models and rule-based systems.

Once deployed, these systems evaluate behavioural data and determine creditworthiness with limited human involvement at the point of decision.

This is visible in MTN’s MoSente product, where loan amounts are determined by usage of mobile services such as airtime, data, SMS, bill payments, and mobile money transactions. Credit limits adjust automatically based on behaviour. No loan officer is involved in these adjustments.

Merchant loan products operate in a similar way. Borrowers are identified through transaction histories and credit bureau data, then directly offered loans. In many cases, there is no application process; customers are selected by the system.

An academic proposal for AI-enabled lending in Uganda’s SACCO sector describes a more advanced model where systems continuously analyse mobile money transactions, utility payments, and behavioural data to build dynamic borrower profiles. These systems integrate national ID databases, mobile APIs, and credit bureaus, and update risk assessments over time.

However, most systems in operation today still rely on periodic model updates rather than continuous autonomous learning.

Uganda’s regulatory framework was not designed for this level of automated decision-making. The Bank of Uganda licenses financial institutions and payment providers, but oversight of proprietary scoring models remains limited. Regulators have acknowledged the importance of innovation while also warning about risks, reflecting a balancing act between inclusion and consumer protection.

According to AI governance expert Nesta Paul Katende, however, the narrative of uncontrolled automation misses a key point.

“We have already deployed agentic credit intelligence within regulated environments in Uganda,” Katende says. “These systems do not operate outside guardrails; the guardrails define their reasoning. Compliance is not an overlay. It is embedded in the way decisions are made’’ he says.

‘’What appears to be a technological leap is, in reality, a governance design challenge. When properly architected, agentic AI delivers tighter control, stronger auditability, and greater accountability than many legacy systems in operation today.”he adds

His argument introduces a different reading of the shift, not as a breakdown of oversight, but as a redesign of how oversight is technically implemented.

Still, policy development continues to lag behind technological change. Financial systems evolve through rapid software updates, while regulation moves through slower institutional processes.

The challenge is compounded by limited AI governance frameworks across the region and gaps in technical capacity within oversight institutions, making it difficult to fully audit complex credit models.

The promise of digital lending is real. Financial inclusion in Uganda has risen to around 70 percent, driven largely by mobile money. There are tens of millions of registered mobile money accounts. Yet fewer than one in five Ugandans access formal credit from regulated institutions. Digital lending has helped fill this gap.

But the distribution of access is uneven. Data-driven systems tend to reward consistent, high-frequency digital behaviour. This benefits salaried workers and active traders, while disadvantaging rural households, seasonal earners, and informal workers with irregular income flows.

These groups are not explicitly excluded, but they are less likely to meet algorithmic risk thresholds.

The result is a form of financial stratification that is difficult to see. A loan officer who rejects an application can explain the decision. An automated system does not. Borrowers often experience silent credit changes or sudden ineligibility without explanation.

Machine learning models are also periodically updated, meaning credit outcomes can shift without formal policy changes. A borrower approved today may be declined later, not because rules have changed, but because the model’s risk interpretation has evolved.

Institutional terms reinforce this imbalance. Providers reserve the right to adjust accounts, offset balances, and report defaults to credit bureaus without prior notice. Borrower obligations are explicit, while transparency obligations remain limited.

This raises a key question of accountability. When an automated system denies credit or changes access, responsibility becomes difficult to assign. It may lie with the bank, the telecom operator, the fintech provider, or the model itself.

Beyond access lies a deeper shift: behaviour shaping. These systems are designed to reduce default risk and improve repayment rates by adjusting credit limits and incentives based on user behaviour.

Over time, access to credit becomes tied not only to income, but to how consistently individuals match machine-defined patterns of reliability. Regular digital activity is rewarded. Irregular income patterns are penalised.

MTN is expanding its mobile money business into a standalone financial services structure, reflecting the growing importance of digital finance. Across Africa, its fintech operations have become a multi-billion-dollar revenue segment. Airtel Money is also scaling its credit offerings, increasing competition in the digital lending space.

Uganda is not alone in this transformation. Across emerging markets, data-driven lending systems are being embedded into financial infrastructure serving populations with limited legal literacy and weak consumer protection systems.

The credit gap is real. So is the demand for financial access. But the systems filling that gap are not neutral. They shape behaviour, define inclusion, and redistribute opportunity in ways that remain largely invisible.

What is emerging is not simply digital banking. It is a redesign of how credit is assigned. The role of the banker is being redistributed into systems that operate continuously and at scale. The institution no longer just lends money, it observes, learns, and decides. The real question is no longer whether these systems work. It is who defines how they work, and who gets to see the rules behind them.