The excitement surrounding Burkina Faso’s recent diaspora bond should not be viewed simply as a financial success story from West Africa. It should force countries such as Uganda to confront a much deeper question about development, agriculture, and the sources of national capital.

Every year, Ugandans living abroad send home enormous sums of money. The figures vary from year to year, but remittances consistently rank among the country’s largest sources of foreign exchange, often exceeding what Uganda receives from some traditional development partners and rivaling major sources of external capital. Yet despite this reality, remittances are rarely discussed as a strategic development asset. They are treated as household income rather than national investment capital.

This raises an important question. If Ugandans abroad already send billions back home every year, why has the country struggled to convert even a fraction of that money into productive capital capable of financing long-term economic transformation?

The answer becomes particularly relevant when one looks at agriculture.

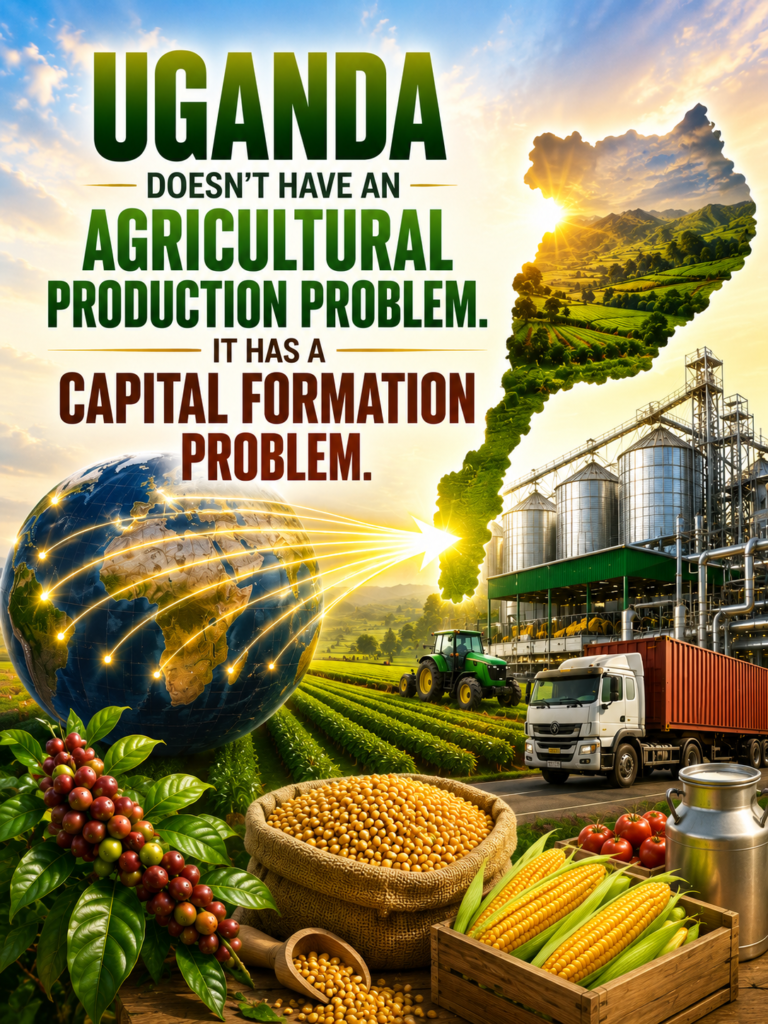

For decades, Uganda’s agricultural debate has been dominated by production. Government programmes, donor projects, development strategies, and political campaigns have largely focused on increasing output. More seeds, more extension services, more mechanisation, more farmers, and more acreage have often been presented as the pathway to transformation.

Yet production is rarely where Uganda’s agricultural system breaks down.

Across the country, farmers are already producing coffee, maize, beans, milk, fruits, fish, poultry, and livestock in significant quantities. The challenge emerges after production. Coffee leaves farms with limited local value addition. Grain is sold immediately after harvest because storage capacity is inadequate. Traders struggle to access affordable working capital. Processors frequently operate below capacity. Export opportunities are missed because supply chains remain fragmented and underfinanced.

As a result, Uganda continues to produce agricultural commodities while capturing only a fraction of the value they create.

This is why the country’s agricultural challenge increasingly appears less like a production problem and more like a capital formation problem.

Uganda possesses fertile land, favourable weather conditions, and entrepreneurial farmers, growing regional demand, and expanding export opportunities. What it often lacks is the patient capital required to organise these advantages into competitive agricultural value chains capable of creating wealth at scale.

Ironically, some of that capital may already exist.

The Ugandan diaspora represents one of the country’s largest pools of untapped financial resources. Beyond the remittances sent to support families, there exists a growing community of professionals, entrepreneurs, investors, and business owners spread across North America, Europe, the Middle East, Asia, and other parts of Africa. Many maintain strong emotional, family, and economic ties to Uganda. Many would like to participate in the country’s growth story.

The challenge has never been patriotism.

The challenge has been creating credible investment vehicles capable of transforming patriotism into productive capital.

Imagine a structure that allows Ugandans abroad to invest directly in strategic grain reserves, commodity aggregation systems, agricultural processing facilities, irrigation infrastructure, export logistics networks, or commodity financing platforms. Such investments would not merely support farmers. They would strengthen entire value chains while generating economic returns for investors and expanding the country’s productive capacity.

This is where the Burkina Faso experience becomes interesting.

The lesson is not that Africa should reject international lenders, foreign investors, or development finance institutions. Uganda will continue to require external capital, and there is nothing inherently wrong with that. The more important lesson is that countries often underestimate the development potential of their own citizens.

People invest where they trust institutions. They invest where governance is transparent. They invest where reporting is credible and where they can clearly understand how value is being created. When those conditions exist, capital tends to follow.

This is ultimately why discussions about agricultural transformation must move beyond production targets and begin focusing on capital mobilisation. The future of Uganda’s agricultural economy will not be determined solely by how much coffee, maize, milk, or grain the country produces. It will be determined by whether sufficient capital exists to aggregate, store, process, transport, finance, and market that production competitively.

The countries that successfully industrialise agriculture are rarely those that produce the most. They are often the ones that mobilise capital most effectively around production.

Burkina Faso’s bond therefore raises a question that Uganda cannot afford to ignore. If millions of Ugandans abroad are already contributing to the economy every year through remittances, what would happen if the country developed trusted mechanisms that allowed them to become investors rather than simply senders of money?

Because the next phase of Uganda’s agricultural transformation may not require more production. It may require a national conversation about how to convert private savings into productive capital. And that is a very different challenge altogether.

Editorial Note: Uganda’s agricultural future will be determined not only by what farmers produce, but by how effectively the country mobilises capital, builds markets, and creates institutions capable of converting production into wealth. This article is part of an ongoing Publicist East Africa series exploring that transition.

Coffee vs Gold: Which Commodity will drive Uganda’s future?