Uganda has set itself one of the most ambitious economic targets anywhere on the African continent: expanding the economy from approximately US$50 billion today to US$500 billion by 2040. If realised, the target would fundamentally alter the country’s economic position within Africa and reshape its role in regional and global markets. Yet behind the headline figure lies a far more difficult question: can Uganda sustain the level of growth needed to get there?

According to the World Bank, achieving this ambition will require Uganda to maintain an average annual economic growth rate of around 10% over the next 15 years. Few countries have managed such a feat over a sustained period. Those that did, including South Korea, Singapore, China and Vietnam, did not simply grow faster; they fundamentally transformed the structure of their economies.

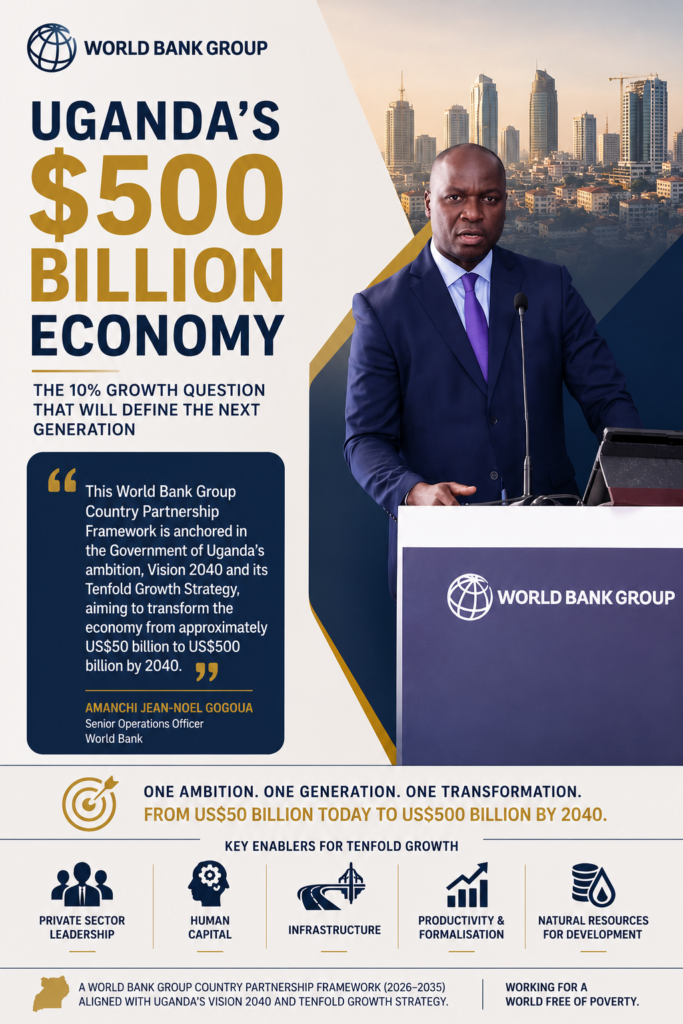

It is against this backdrop that the World Bank launched its Country Partnership Framework (2026–2035) alongside the Uganda Public Finance Review in Kampala, positioning the framework as a strategic blueprint aligned with Uganda’s Vision 2040 and the Government’s Tenfold Growth Strategy.

Speaking at the launch, World Bank Senior Operations Officer Amanchi Jean-Noel Gogoua underscored both the scale of the ambition and the role of the private sector in achieving it.

“This World Bank Group Country Partnership Framework is anchored in the Government of Uganda’s ambition, Vision 2040 and its Tenfold Growth Strategy, aiming to transform the economy from approximately US$50 billion to US$500 billion by 2040.” he said.

He added that the overarching objective of the framework is to advance private sector-led socioeconomic transformation capable of creating more and better jobs.

The announcement is significant not merely because of the size of the target, but because it reflects a shift in how Uganda must think about growth. For decades, the country has been among East Africa’s more resilient economies. Agriculture, services, construction and public investment have sustained respectable expansion, while prudent macroeconomic management has enabled Uganda to weather regional and global shocks better than many of its peers.

However, sustaining annual growth of 10% belongs to an entirely different category of economic performance. Resilience alone will not deliver it, nor will incremental improvements to existing industries. The countries that successfully maintained double-digit growth fundamentally changed how they created value. Labour moved from low-productivity agriculture into manufacturing and modern services. Domestic firms became exporters. Infrastructure expanded rapidly. Capital flowed into productive industries, while governments invested heavily in education, technology and institutions capable of supporting industrialisation.

Uganda therefore faces a challenge that is larger than increasing GDP. It must become a fundamentally different economy.

The encouraging news is that Uganda enters this period with several advantages. Commercial oil production is expected to commence in 2027, potentially providing the government with significant new revenues to finance long-term development. At the same time, Uganda possesses one of the youngest populations in the world, with nearly three-quarters of its citizens below the age of 30 and an estimated 650,000 young people entering the labour market every year.

For many economists, this combination of natural resources and demographics represents a once-in-a-generation opportunity. As Gogoua observed, Uganda stands at a critical inflection point. Oil could lift economic growth beyond 6.5%, while the country’s youthful population could become one of its greatest competitive advantages.

Yet demographics alone do not generate prosperity. Young people become an economic dividend only when they are educated, skilled and absorbed into productive sectors of the economy. Without that transition, a demographic dividend can quickly become a demographic challenge.

At the centre of Uganda’s transformation lies one defining concept: productivity. Every country that has achieved rapid economic development has dramatically increased the amount of value produced by each worker, each business and each unit of capital. That is what separates developing economies from industrial economies. It is the difference between exporting raw coffee and exporting branded consumer products; between subsistence farming and commercial agribusiness; and between informal trading and globally competitive manufacturing.

Uganda’s challenge becomes clearer when viewed through this lens. According to the World Bank, 92% of Ugandan workers remain in informal employment. While the informal economy provides livelihoods for millions of households, it also limits productivity, tax mobilisation, business financing and technological adoption. Businesses operating outside formal systems often struggle to access credit, attract investment or scale beyond local markets. Formalisation is therefore not simply a taxation issue, it is a productivity strategy.

Human capital presents an equally significant challenge. The World Bank notes that Uganda’s Human Capital Index stands at 0.39, meaning that a child born today is expected to realise only 39% of his or her productive potential because of shortcomings in education and healthcare. This is more than a social development concern; it represents billions of dollars in unrealised economic output. No country has successfully industrialised without investing heavily in engineers, technicians, researchers, healthcare professionals, entrepreneurs and digitally skilled workers. Human capital is no longer simply a welfare issue, it is one of the most important drivers of national competitiveness.

Infrastructure remains another critical constraint. The World Bank estimates that only 9% of Ugandans currently have access to the national electricity grid, while digital connectivity stands at approximately 50%. At the same time, non-oil tax revenues remain around 13.5% of GDP, limiting the government’s fiscal capacity to finance major investments. These figures illustrate an important reality: electricity is no longer merely a public utility, it is industrial infrastructure.

Broadband is no longer simply about communication, it is economic infrastructure. Efficient transport networks, logistics systems and reliable energy determine whether manufacturers can compete in regional and international markets. Without these foundations, even the most ambitious industrial policies struggle to deliver sustained productivity gains.

Commercial oil production could provide Uganda with substantial new fiscal resources, but history offers an important lesson. Natural resources have created lasting prosperity only where governments invested those revenues into productive assets such as education, infrastructure, industrialisation and innovation rather than financing consumption alone. Norway transformed oil wealth into one of the world’s largest sovereign wealth funds.

Botswana invested diamond revenues into strong institutions and public services. Others failed to convert resource wealth into sustainable development. For Uganda, oil should therefore be viewed as an accelerator of economic transformation, not as the transformation itself.

Perhaps the most important question for business leaders is not whether Uganda can reach a US$500 billion economy, but where the additional US$450 billion will come from. The answer is unlikely to lie in existing industries simply producing more of the same. Instead, Uganda’s next phase of growth will almost certainly be driven by sectors capable of generating significantly higher productivity, value addition and export earnings. Agro-processing must replace raw commodity exports with branded products. Manufacturing must expand beyond domestic demand into regional and international markets. Oil and gas must stimulate wider industrial development through local content and downstream industries.

Technology companies will need to create scalable digital services, while tourism must evolve into a higher-value experience economy. Financial markets, pension funds and development finance institutions will have to mobilise the patient capital required to finance factories, logistics infrastructure, renewable energy projects and export-oriented businesses. These are not simply policy priorities; they represent the country’s most significant investment opportunities.

One of the strongest messages emerging from the World Bank’s framework is its emphasis on private sector-led growth. Governments do not create tenfold economies on their own. Businesses invest capital, create jobs, commercialise innovation, enter export markets and build globally competitive industries. The government’s responsibility is to create the enabling environment through sound policy, quality infrastructure, effective institutions and predictable regulation. When those conditions exist, private enterprise becomes the engine of transformation.

Ultimately, Uganda’s ambition to become a US$500 billion economy is not simply a question of arithmetic. It is a question of economic transformation. Can millions of workers move into higher-productivity employment? Can businesses produce more sophisticated goods and services? Can education prepare the workforce required for an industrial economy? Can financial markets finance long-term investment rather than short-term consumption? Can infrastructure support globally competitive manufacturing and exports?

These are the questions that will determine whether Vision 2040 becomes reality.

The countries that achieved sustained double-digit growth did not simply expand their economies, they reinvented them. Uganda now stands at a similar crossroads. Vision 2040 is no longer just a government aspiration; it is a national economic proposition that demands coordinated action from policymakers, investors, financiers and business leaders alike. Whether the country reaches a US$500 billion economy will depend less on the scale of its ambition than on the speed with which it transforms how it creates value. That is the real challenge behind the tenfold growth vision, and ultimately, the measure by which its success will be judged.