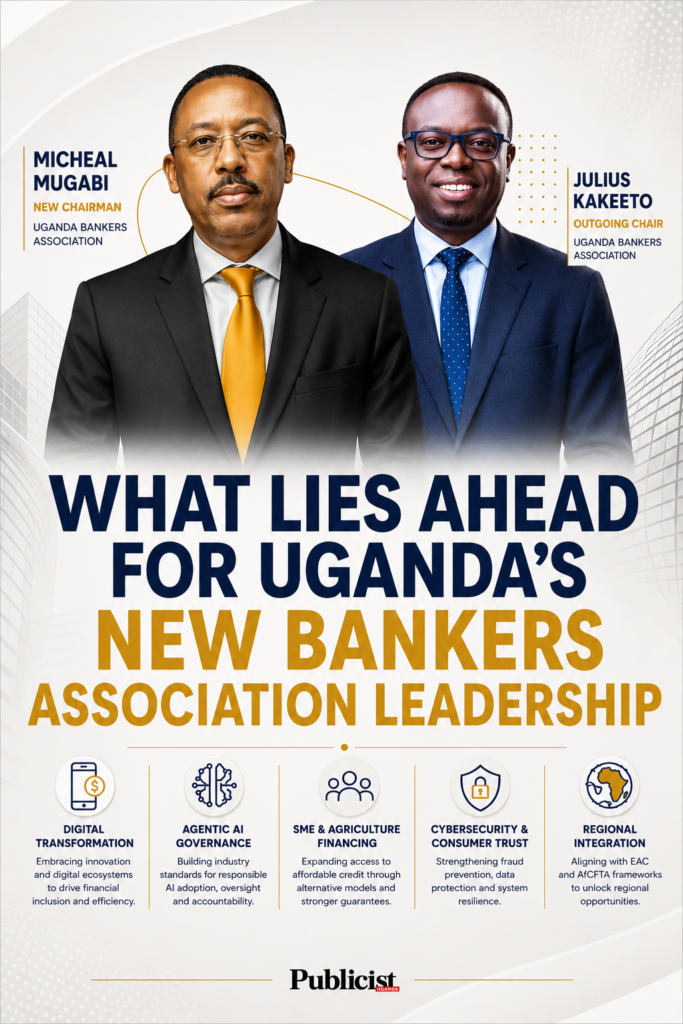

The transition in leadership at the Uganda Bankers Association comes at a pivotal moment for Uganda’s financial sector, defined by accelerating digital disruption, tightening macroeconomic conditions, rising credit risks, expanding regional integration, and the rapid emergence of artificial intelligence as a structural force in global banking.

Far from a routine institutional handover, the new leadership inherits a banking environment undergoing deep transformation.

Private sector credit growth has remained uneven, constrained by risk perceptions, inflationary pressures, and cautious lending to agriculture and SMEs. Meanwhile, digital financial services continue to redefine financial inclusion.

The GSMA’s State of the Industry Report estimates that Sub-Saharan Africa accounts for more than 75 percent of global mobile money transaction activity, underscoring a structural shift in how financial services are accessed and delivered.

Nowhere is this truer than in Uganda itself. MTN MoMo and Airtel Money have built an entrenched duopoly, until recently commanding the landscape before a Bank of Uganda update in late 2025 revealed 54 licensed payment service providers reshaping the competitive order.

In 2025, MTN disbursed Shs 2.7 trillion in mobile loans to 3.4 million borrowers, with the average Ugandan taking multiple small loans per year. These are not supplemental services: for the informal trader in Owino Market or the boda boda operator in Gulu, mobile money has become the primary financial infrastructure of daily life.

Formal banks, by contrast, remain largely a tool for salary recipients, urban businesses, and the formally employed. As a result, banks are increasingly transitioning from primary transaction processors to liquidity providers and infrastructure nodes within broader digital ecosystems, shifting competitive dynamics from bank-versus-bank rivalry to ecosystem-versus-ecosystem competition.

One of the most consequential emerging forces is the rise of agentic artificial intelligence, AI models capable of executing financial tasks autonomously in real time.

A 2025 McKinsey Global Institute report estimates AI could generate up to $340 billion annually in value for global financial services, driven by automation in credit underwriting, fraud detection, compliance, and customer engagement. However, this transformation introduces complex governance challenges, including algorithmic accountability, explainability of automated decisions, and systemic risk from interconnected AI systems.

For the Uganda Bankers Association, this implies coordinated industry standards on AI governance, shared risk frameworks, and clear data protection protocols across member banks.

Structural challenges persist alongside these technological shifts. SMEs account for over 80 percent of private sector employment in Uganda, yet access to affordable credit remains constrained by weak credit data infrastructure and underdeveloped collateral systems.

The problem is compounded by Uganda’s predominantly agricultural economy, where smallholder farmers face seasonal income cycles that formal credit scoring systems are not designed to accommodate, and where land tenure disputes continue to undermine collateral-based lending.

The 2025 banking sector report showed non-performing loans falling from 4.8 percent to 3.4 percent, a positive sign, but the agriculture and informal sectors remain structurally underserved, creating a clear imperative for industry-wide coordination on alternative credit models and stronger credit guarantee frameworks.

There is also the uncomfortable reality of Uganda’s low penetration of insurance and long-term savings. Formal savings as a share of GDP remain thin, pension coverage is limited largely to formally employed workers, and insurance products have struggled to reach the mass market, leaving households and businesses without meaningful buffers against shocks.

This gap constrains the very deposit base that banks rely on for credit expansion, and represents an area where UBA advocacy and product innovation could generate systemic gains.

Uganda’s financial system is also increasingly embedded within regional frameworks, the East African Community and the African Continental Free Trade Area, meaning competition, regulation, and opportunity are now regional in nature.

At the same time, rising digital fraud across African banking and mobile money systems places growing emphasis on cybersecurity resilience and consumer protection, where trust is not merely a reputational issue but a structural requirement for system stability.

The Financial Sector Anti-Fraud Consortium, launched under Julius Kakeeto’s outgoing tenure, integrating MTN MoMo, Airtel Money, regulators, and law enforcement, represents the kind of collaborative architecture the new leadership must now scale and deepen.

Taken together, these developments point to a sector in transition, where traditional banking is being redefined by technology, regional integration, and macroeconomic restructuring.

In this environment, the Uganda Bankers Association must evolve from a coordinating industry body into a strategic ecosystem governance platform, shaping shared standards on artificial intelligence, digital finance interoperability, SME credit infrastructure, and cybersecurity.

The effectiveness of the new leadership will ultimately be measured not by industry representation alone, but by its capacity to build a coordinated, resilient, and future-ready financial system capable of navigating technological disruption and macroeconomic transformation simultaneously.