For years, discussions about Uganda’s digital economy have largely centred on internet penetration, mobile money adoption and expanding broadband infrastructure. Yet a quieter transformation has been unfolding beneath the surface, one that suggests the country’s digital future may be financed not by traditional banks, but by smartphones.

M-KOPA Uganda‘s announcement that it has unlocked more than Shs1 trillion in cumulative credit for over one million customers since entering the Ugandan market in 2013 is more than a corporate milestone. It offers a glimpse into how access to productive digital assets is reshaping financial inclusion and economic participation.

Unlike conventional consumer electronics, smartphones have increasingly become tools of production. They enable traders to reach customers through social media, boda boda riders to access ride-hailing platforms, mobile money agents to transact, farmers to obtain market information and young entrepreneurs to build businesses with little more than an internet connection.

The significance of this shift lies not simply in device ownership but in what ownership enables.

According to M-KOPA’s independently validated 2025 Impact Report, 53 percent of surveyed customers acquired their first smartphone through the company’s financing model. More notably, 86 percent say they now use their smartphones to generate income, while 75 percent report earning more since joining the platform. These figures suggest that smartphones are increasingly functioning as productive assets rather than discretionary consumer purchases.

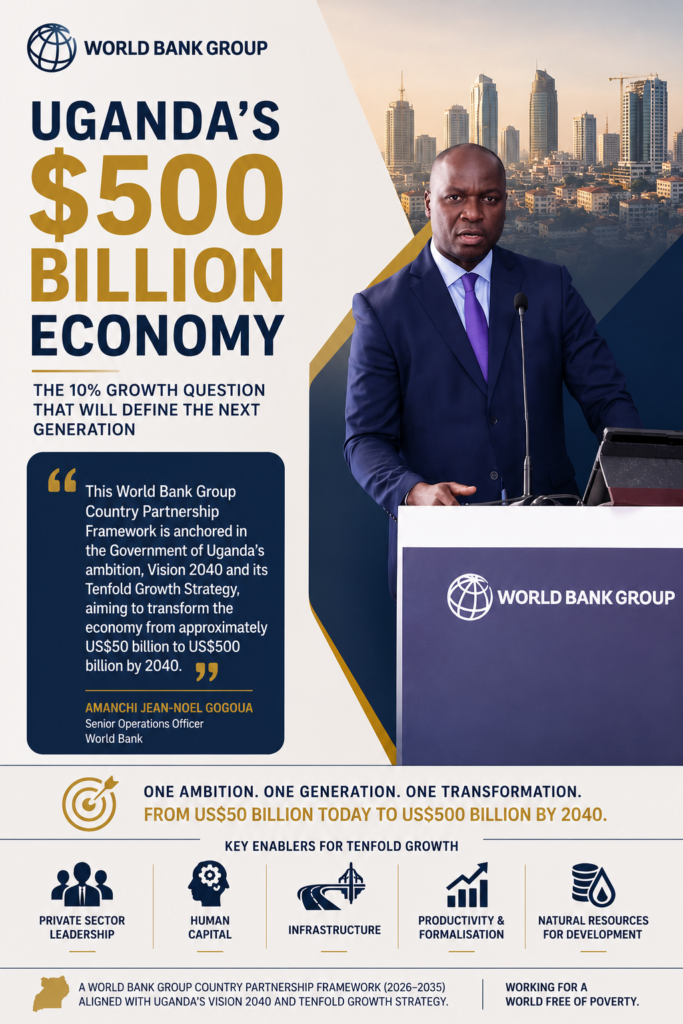

For policymakers pursuing Uganda’s ambition of building a US$500 billion economy by 2040, this trend deserves attention. Digital transformation is often framed around infrastructure investment and connectivity. Equally important, however, is ensuring that ordinary Ugandans can afford the devices through which they participate in that digital economy.

Speaking during the launch of the report, Brendah Nambalirwa-Tzadok, General Manager of M-KOPA Uganda, said the milestone reflects changing perceptions of what smartphones represent for everyday earners.

“Reaching over Shs1 trillion in unlocked credit reflects the trust our customers have placed in M-KOPA over the past decade” she said.

” It also shows that access to smartphones is no longer only about connectivity. For many customers, it is directly linked to income generation, financial inclusion, and everyday opportunity.” she adds.

Her remarks underscore a broader evolution taking place across Africa’s fintech landscape. Increasingly, companies are not merely financing products; they are financing access to economic opportunity.

That evolution is evident in M-KOPA’s latest product strategy. Alongside the impact report, the company introduced two new benefits for customers who complete repayment of their smartphones: discounted upgrades through the M-KOPA app and a trade-in programme allowing customers to exchange existing devices for newer models without an upfront deposit.

These additions complement existing services such as cash loans, free daily data, screen repair and hospital insurance, signalling a shift away from one-off device sales towards long-term digital ecosystems.

The implications extend beyond one company. Uganda has spent years working to deepen financial inclusion, traditionally measured through bank accounts and mobile money wallets. But fintech firms are demonstrating another pathway: financing productive digital assets that help individuals generate income, build repayment histories and access broader financial services over time.

” It also shows that access to smartphones is no longer only about connectivity. For many customers, it is directly linked to income generation, financial inclusion, and everyday opportunity.”

M-KOPA’s wider economic footprint also reflects this growing role. The company says it contributed more than Shs20 billion in taxes in 2024, spent over Shs120.8 billion on local procurement, and supports a network of more than 3,500 agents across the country, creating thousands of earning opportunities.

These figures reinforce an important point. The digital economy is not sustained by technology alone. It depends on financing models that lower barriers to participation and enable millions of people to access the tools required to compete in increasingly digital markets.

As Uganda accelerates its digital transformation agenda, the country’s next phase of economic inclusion may depend less on expanding bank branches than on ensuring that productive technologies remain within reach of everyday earners.

The smartphone, once viewed primarily as a communication device, is quietly becoming one of Uganda’s most important instruments of economic participation. And the financing behind it may prove just as consequential as the technology itself.