For decades, East Africa has occupied a curious position in the global energy economy. The region possesses significant petroleum resources, strategic ports and one of the world’s fastest-growing consumer markets, yet it continues to import most of the refined fuels that power its economies. While crude oil has promised prosperity, much of the value from refining, petrochemicals and downstream manufacturing has remained elsewhere.

Viewed in this context, Kenya’s project should not simply be interpreted as a threat to Uganda’s ambitions. Instead, it raises the level of competition and highlights what will ultimately determine success in the region’s energy sector.

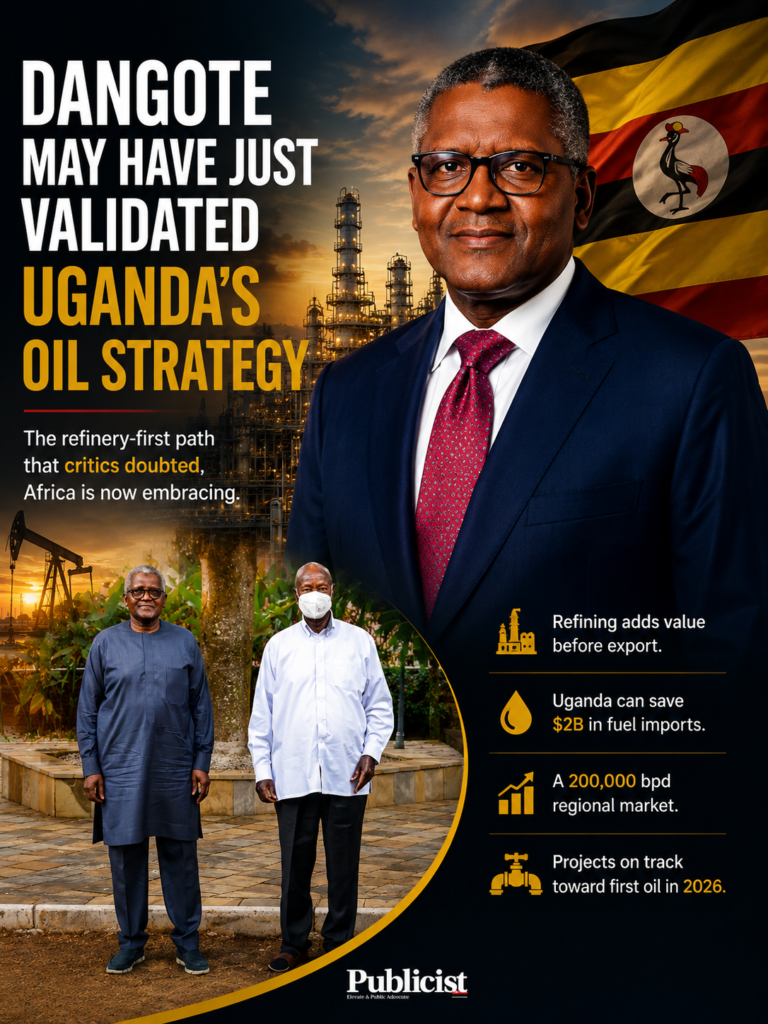

That may be beginning to change. Aliko Dangote, the Nigerian billionaire behind Africa’s largest privately owned industrial group, has confirmed plans to build a $17 billion oil refinery on Lamu Island, off Kenya’s northern coast, financed through internally generated cash, corporate bonds and a future initial public offering. The facility is designed for a capacity of 700,000 barrels per day, larger than the 650,000-bpd Dangote Petroleum Refinery outside Lagos, currently Africa’s largest operating refinery. Soil testing and preliminary engineering work are already under way, with construction expected to take between 30 months and three years. And according to the Kenyan President William Ruto, It is expected to create 60,000 youth jobs.

If realised, it would rank among the continent’s largest privately financed industrial investments and could redefine East Africa’s energy landscape.

Yet the significance of the proposal extends far beyond Kenya. It signals that East Africa is entering a new phase of industrial competition where success will be measured not simply by who produces crude oil, but by who refines it, transports it, manufactures with it and captures the greatest share of value from the petroleum economy.

That distinction is important. For decades, many African oil-producing countries exported crude only to import petrol, diesel, aviation fuel and other refined products at a premium. This model has left economies vulnerable to global price shocks, shipping disruptions and foreign exchange pressures while exporting jobs and industrial opportunities that could have been created locally.

The commissioning of the Lagos refinery has already begun to challenge that model, helping turn Nigeria from a chronic importer of refined fuel into a growing exporter. A second investment of even greater scale in East Africa would reinforce a broader continental shift towards domestic value addition and industrialisation.

The timing is particularly significant because East Africa’s petroleum sector is approaching a defining moment.

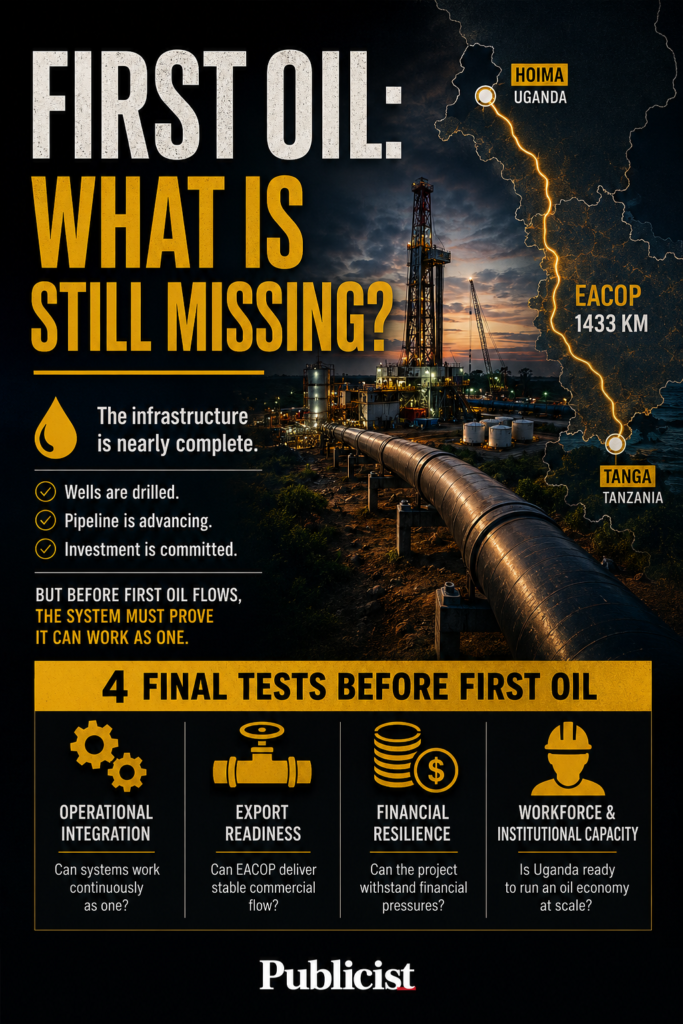

Uganda expects first commercial oil production in 2026 from the Tilenga and Kingfisher projects, with peak production projected at approximately 230,000 barrels per day. Supporting this ambition is the 1,443-kilometre East African Crude Oil Pipeline (EACOP), designed to transport up to 246,000 barrels per day from Hoima in western Uganda to the Port of Tanga in Tanzania.

Uganda’s own refinery, planned for Kabaale in Hoima District, is designed to process 60,000 barrels of crude oil per day. Although significantly smaller than the proposed Kenyan facility, it serves a different strategic objective. Beyond supplying domestic fuel, it is intended to support petrochemicals, bitumen, liquefied petroleum gas and other downstream industries while strengthening the country’s long-term energy security.

Tanzania also remains central to this evolving landscape. As host of the EACOP export terminal at Tanga, a site that was itself briefly considered for Dangote’s East African refinery before talks moved to Kenya, the country occupies a strategic position within the region’s oil value chain while continuing to invest in natural gas, electricity generation and port infrastructure.

Viewed in this context, Kenya’s project should not simply be interpreted as a threat to Uganda’s ambitions. Instead, it raises the level of competition and highlights what will ultimately determine success in the region’s energy sector.

Refining is no longer just an engineering project; it is a test of economic competitiveness. Countries seeking to become regional energy hubs must offer efficient logistics, predictable regulation, competitive financing, reliable infrastructure and access to expanding markets. Investors committing billions of dollars will compare operating costs, transport networks, market demand and policy stability before making long-term decisions.

Kenya enters this competition with clear advantages. The Port of Mombasa is East Africa’s busiest maritime gateway and already serves as the principal entry point for petroleum products destined for Uganda, Rwanda, South Sudan and parts of eastern Democratic Republic of Congo. A large-scale plant integrated into this logistics network, alongside the Lamu site itself, could significantly strengthen Kenya’s position in regional fuel supply and downstream manufacturing. The Kenyan government has signalled its own stake in the outcome, designating seed capital of roughly Ksh 21.5 billion towards the project.

Uganda’s comparative advantage lies elsewhere. With an estimated 6.5 billion barrels of oil in place, including around 1.4 billion barrels considered recoverable, the country possesses the resource base to support long-term industrial development. Combined with EACOP and the planned Kabaale refinery, Uganda has an opportunity to build an integrated petroleum economy that extends beyond crude exports into higher-value manufacturing.

Tanzania also remains central to this evolving landscape. As host of the EACOP export terminal at Tanga, a site that was itself briefly considered for Dangote’s East African refinery before talks moved to Kenya, the country occupies a strategic position within the region’s oil value chain while continuing to invest in natural gas, electricity generation and port infrastructure.

Rather than creating a winner-takes-all contest, these investments could establish complementary strengths across the region. Uganda provides crude oil production, Kenya offers logistics and now potentially large-scale refining, while Tanzania serves as a critical export and energy corridor. Together, they have the potential to reduce East Africa’s dependence on imported refined petroleum products and strengthen regional energy security.

Equally significant is what Dangote’s plans reveal about infrastructure finance in Africa. Large industrial projects have traditionally depended on government borrowing or sovereign guarantees. However, as fiscal pressures increase across the continent, private capital is becoming increasingly important. Dangote’s intention to finance the Kenya project through corporate cash flows, bond markets and a future public listing reflects a growing trend towards privately funded infrastructure.

That said, the Lagos precedent is a useful caution against taking the $17 billion figure as final. That refinery was originally budgeted at roughly $9 billion in 2013 but eventually cost more than $20 billion, after a site relocation, engineering setbacks, currency depreciation, the pandemic and global inflation pushed costs well beyond initial estimates. If the Kenya project follows a similar trajectory, both the price tag and the financing structure behind it should be expected to shift before completion.

This shift matters because Africa’s infrastructure financing gap remains substantial. The African Development Bank estimates that the continent requires between US$130 billion and US$170 billion in infrastructure investment annually, leaving a financing gap of US$68 billion to US$108 billion each year. Mobilising private capital will therefore be essential if Africa is to accelerate industrialisation without placing unsustainable pressure on public finances.

Ultimately, the refinery race unfolding in East Africa is about much more than petroleum. It is about where industries are built, where value is added and where economic transformation takes place.

Countries that merely extract natural resources rarely achieve sustained industrial growth. Those that process those resources, develop manufacturing ecosystems and integrate into regional value chains capture far greater economic benefits through employment, technology transfer and export diversification.

Dangote’s Kenya investment should therefore be seen as more than another refinery announcement. It is a reminder that Africa’s next phase of development will be driven not only by the resources beneath its soil but by the industries built above it.

For Uganda, Kenya and Tanzania, the challenge is no longer simply to produce oil. It is to create competitive industrial ecosystems capable of transforming natural resource wealth into long-term prosperity. That, not the size of any single refinery, will determine who leads East Africa’s next chapter of economic growth.